Investing Backwards: The Mistake Most DIY Investors Make

Over the years I have sat across from a lot of capable, intelligent people who manage their own investments. They tend to be successful in their careers, disciplined with their money, and genuinely engaged in their financial lives. And yet many of them are making the same quiet mistake. It has nothing to do with intelligence and everything to do with the order in which they do things.

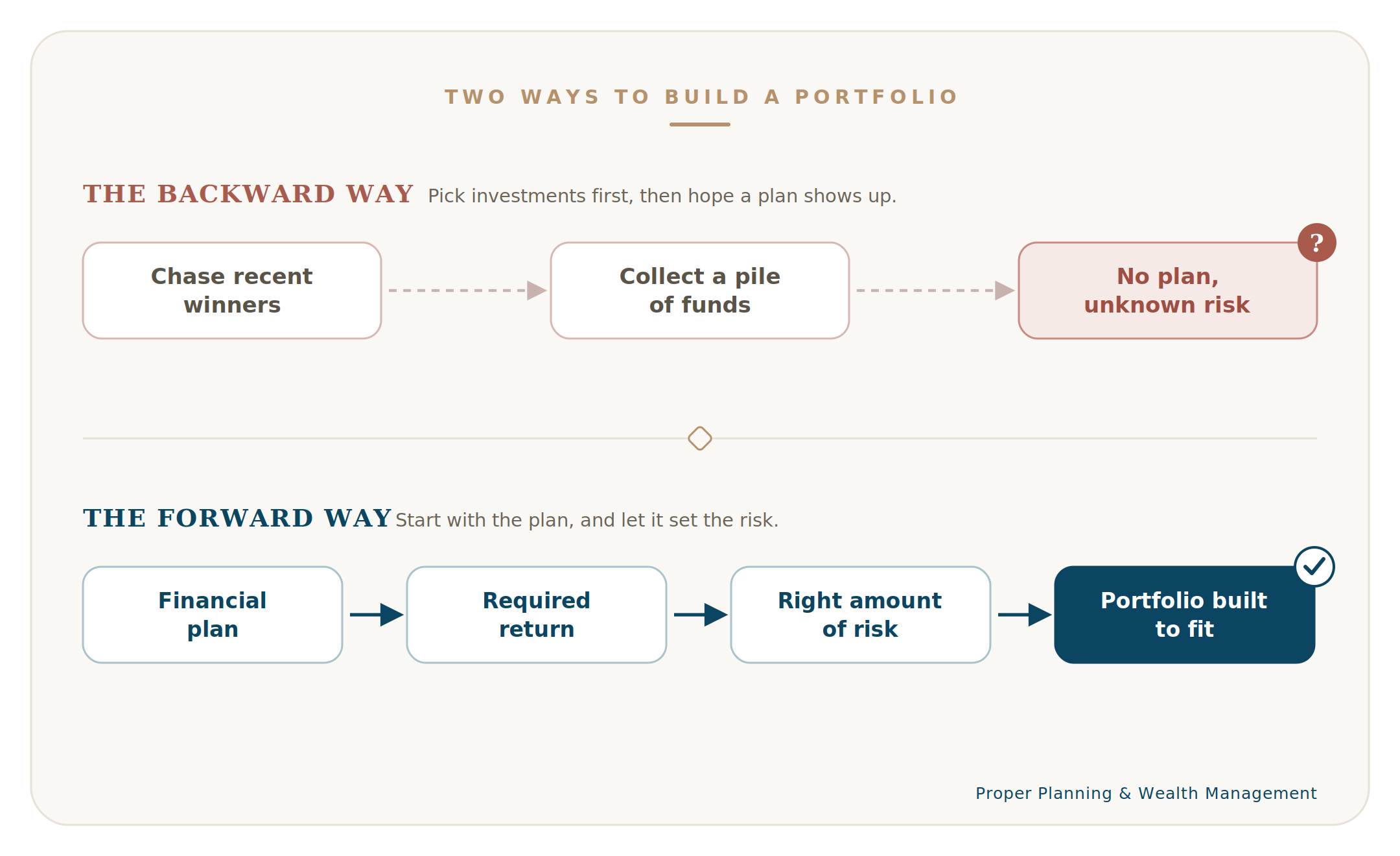

They build a portfolio first and look for a plan later. The better approach runs in exactly the opposite direction.

Steering by the rearview mirror

When most do-it-yourself investors decide where to put their money, they start by looking at what has done well recently. They pull up a list of the top performing funds over the last three, four, or five years and they buy the winners. It feels logical. If something has been going up, why would you not want to own it?

The trouble is that you are steering the car by staring into the rearview mirror. Trailing performance tells you where an investment has already been, not where it is headed. Markets move in cycles, and the leaders of one cycle are often lagging in the next. The fund that looks irresistible today usually looks that way because it has already had its run.

A collection of funds is not a portfolio

This next one is more subtle. Even an investor who picks several genuinely good funds can end up with a portfolio that does not hold together.

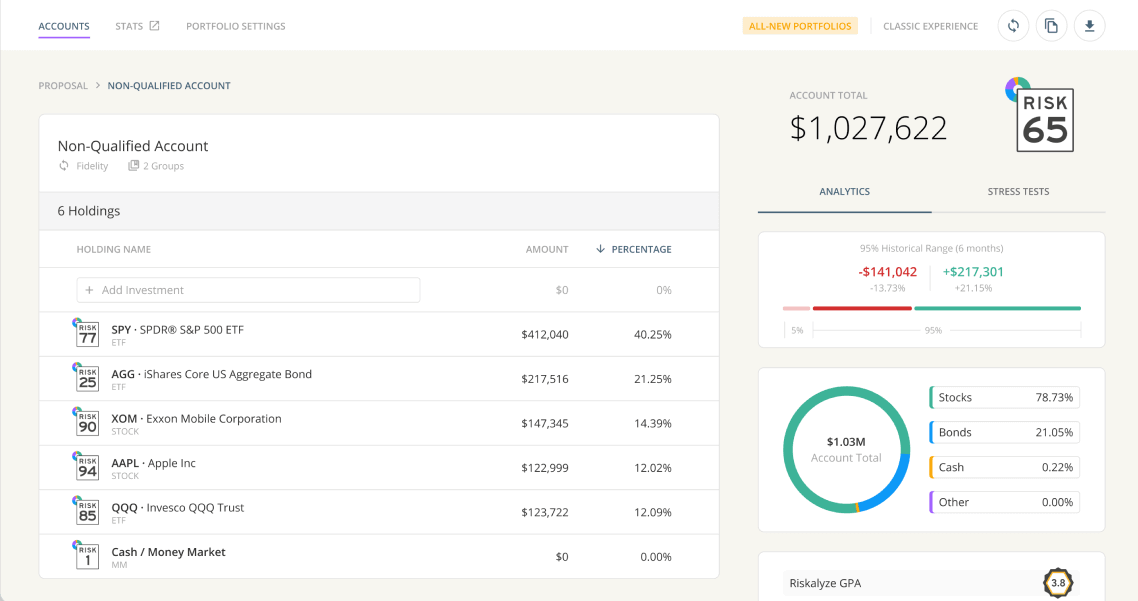

Think of it like cooking. You can buy five excellent ingredients and still not have a meal. A true portfolio is a recipe, not a shopping cart. The pieces have to work together. When you assemble holdings one at a time, each because it looked good on its own, you frequently end up with funds that own many of the same companies, stack the same risks on top of one another, and move in the same direction at the same time. You feel diversified because you own a lot of different tickers, but under the surface you are concentrated and exposed in ways you never intended. When we run a portfolio like that through Nitrogen, the platform we use to analyze how risky a portfolio truly is, the hidden overlap and correlation usually show up fast, and people are often surprised by how much risk they were carrying without realizing it.

The question almost no one asks

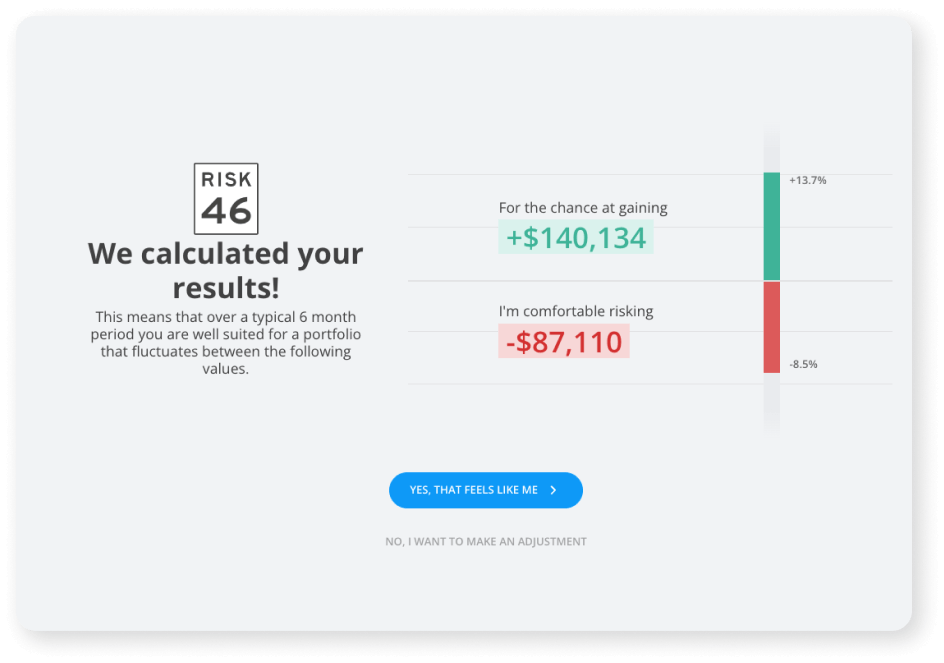

Here is the part that gets skipped entirely. How much risk should you be taking in the first place?

Most DIY portfolios have no answer to that question, because there is nothing to measure the risk against. Risk is taken on instinct, or based on how confident the market felt that month, or simply as a byproduct of chasing returns. Without a destination, there is no way to know whether you are taking too much risk, too little, or close to the right amount. You are accelerating without knowing where you are trying to go.

This is one place where the right tools earn their keep. We use a Risk Tolerance Questionnaire to put an actual number on two things that usually go unmeasured, the level of risk you are comfortable taking, and the level of risk your current portfolio is actually carrying. Most of the time, the two do not line up.

Why chasing winners quietly works against you

Performance chasing does more than expose you to the next cycle’s losers. It also tends to cost you money in a way that is easy to miss.

Each year, Morningstar publishes a study called Mind the Gap (click here to view) that compares the returns a fund actually produced with the returns its investors actually earned. You might think they are the same, but they're not. When looking up a fund, you'll see the total returns that assume you bought once and held on. Investors, on the other hand, tend to add money after things have gone up and pull money out after things have gone down.

In the most recent study, covering the ten years through the end of 2024, Morningstar found that the average dollar invested in US funds and ETFs earned roughly 7% per year, while the funds themselves returned about 8.2%. That is a gap of around 1.2% every year, due to the timing of when investors bought and sold. Over a decade, that works out to about 15% of the available return left on the table. Morningstar describes it as a persistent cost, not unlike an expense ratio, except this one is entirely self-inflicted and largely avoidable.

Build forward, not backward

So what does building a portfolio in the right order actually look like?

It starts with a plan, not a fund list. Before a single investment is chosen, the real questions get answered. When do you want to retire, or reach financial independence? How much income will you need, and for how long? What do you want to leave behind, and for whom? What major expenses sit between here and there?

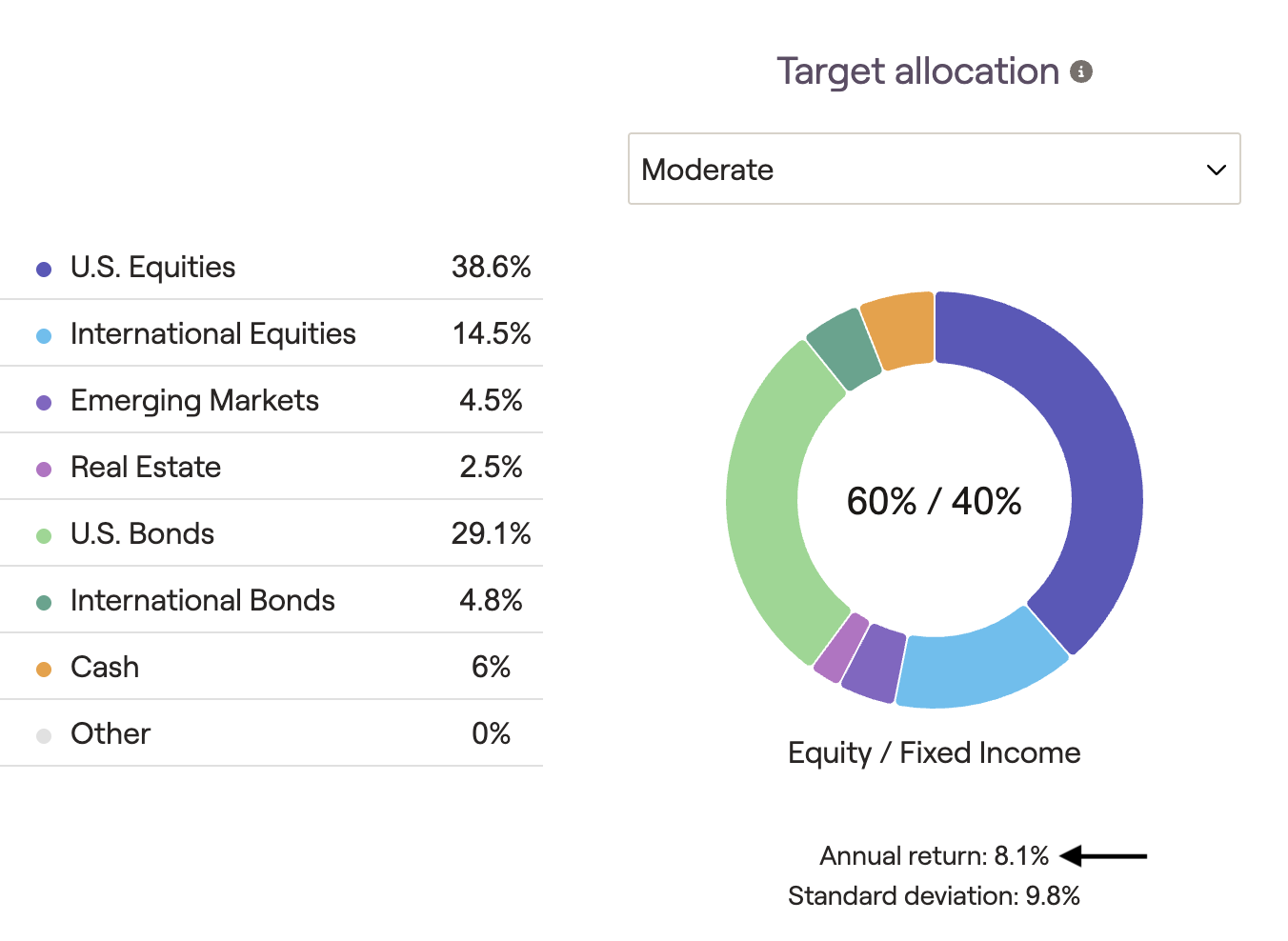

Those answers dictate how we build your financial plan, and a well-built plan produces something most DIY investors never calculate... a required rate of return. In other words, the plan tells you how hard your money actually needs to work in order to fund the life you are describing. That number changes everything, because now risk is no longer a guess. The required return tells you how much risk you need to take, and only then do you build a portfolio designed to take that amount of risk as efficiently as possible.

Plan first. The plan sets the required return. The required return sets the risk. The risk sets the portfolio. That is the sequence, and it is the reverse of how most people do it.

Take the least risk necessary

This is the part I hope you take with you. The goal of investing is not to earn the highest possible return. The goal is to reach your goals while taking the least risk necessary to get there.

If your plan works comfortably at a 6% assumed return, there is no prize for reaching for 9. You would simply be taking on volatility, drawdowns, and sleepless nights you do not need, and giving the behavior gap more room to do its damage. A good plan does not ask how much you can make. It asks how little risk you can take and still arrive where you want to go. That is a far more lasting, and far more peaceful, way to invest.

A better starting point

If you have been building your portfolio the way most people do, by collecting whatever looked best lately, you are in good company, and you are not stuck there. The fix is not a hot new fund or a better forecast. It is a change in order of operations: a plan first, and a portfolio built to serve it.

That is the work we do at Proper Planning & Wealth Management. If you would like to see what your own required return looks like, and how much risk you actually need to take to reach your goals, we would be glad to walk through it with you.

We also offer prospective clients a complimentary risk analysis using Nitrogen. It is a clear, jargon-free way to see how much risk you are currently taking, how that compares to the level of risk you are actually comfortable with, and the range your portfolio would be expected to move within during a normal year. We can also stress test your holdings against real historical events, such as the 2008 financial crisis, the dot-com crash, and the 2013 taper tantrum, to show how your portfolio would have held up, along with how correlated your investments truly are. For most people, it is the first time they have seen all of that in one place. If that sounds useful, reach out and we will set it up.

Does your portfolio deserve a risk management analysis?

All investments carry risk, including the possible loss of principal. Past performance is not indicative of future results. Diversification does not guarantee against loss. This article is for educational purposes and does not constitute investment, tax, or legal advice.