Are You Getting the Most From Your Garmin Benefits?

I work with a number of Garmin employees in Olathe and the Kansas City area, and one thing comes up again and again: Garmin offers one of the strongest benefit packages I have seen, and a lot of people are not capturing everything available to them. The good news is that fixing this rarely requires earning more or saving dramatically more. It usually just requires understanding how the pieces fit together. Here is where I focus when a Garmin employee sits down with me for the first time.

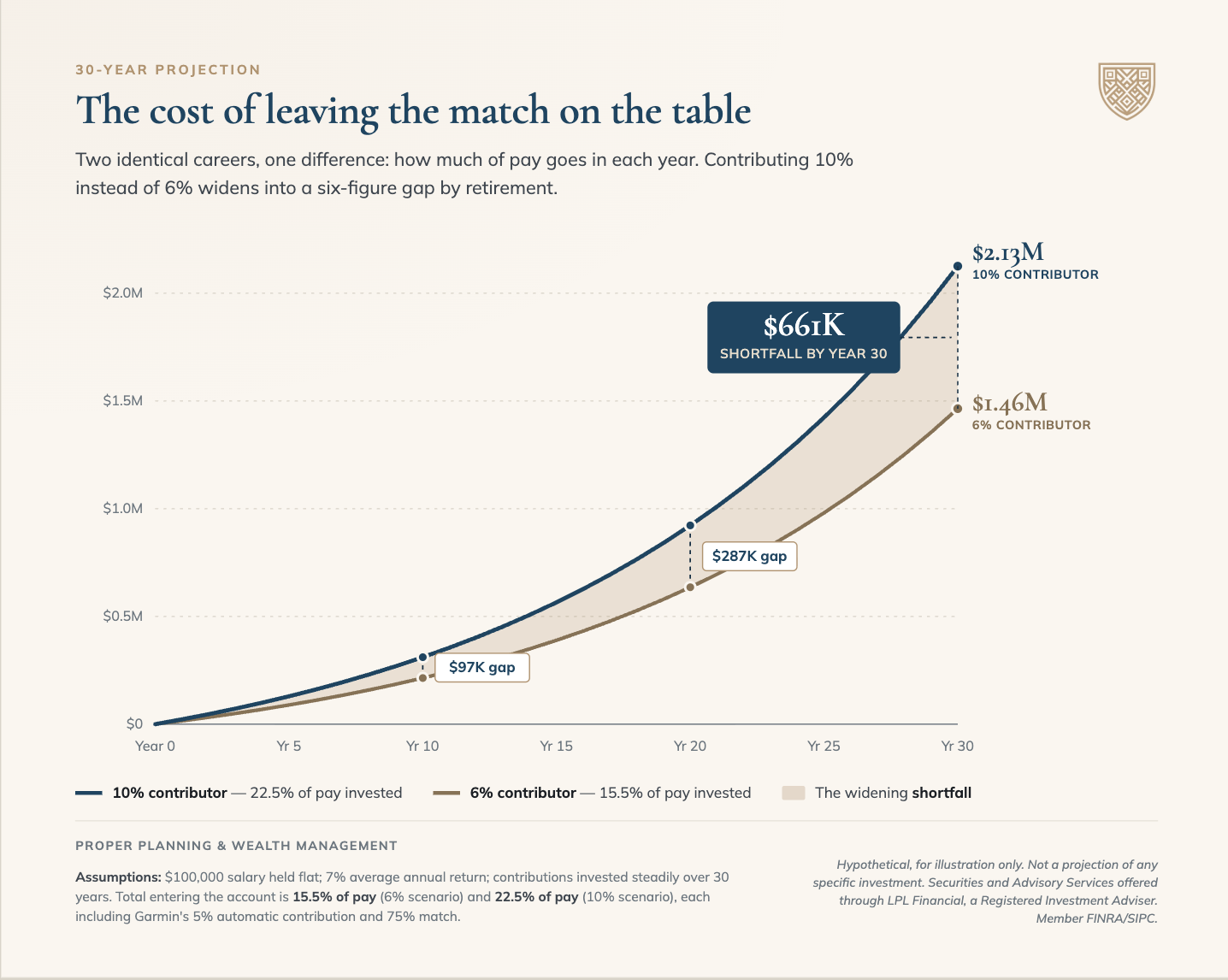

Start With the 401k Match

Garmin contributes 5% of pay to every employee's 401k automatically, then adds a 75% match on the first 10% of salary you contribute. Put those together and an employee contributing at least 10% receives a total employer contribution of 12.5% of pay. That is extraordinary, and yet I regularly meet long-tenured employees contributing 6% who have never done the math on what they are giving up.

The gap compounds. When I show someone the difference between contributing 6% versus 10% over a 20 or 30 year career, with market growth layered on top, the shortfall can easily reach six figures. If you do nothing else after reading this, confirm you are contributing enough to capture the full match.

The ESPP and Its Built-In Discount

Garmin's Employee Stock Purchase Plan includes a lookback provision. Shares are purchased at a 15% discount off the lower of the price at the beginning or the end of the plan period. That combination is not common, and it’s very favorable to the employees.

The catch is what happens next. I see ESPP shares sitting untouched in brokerage accounts for years, quietly growing into a large position that no one has a plan for. There are real tax considerations around when you sell, and there is real risk in letting a single stock become a major piece of your net worth. A discount on the purchase is only valuable if you also have a strategy for the shares afterward.

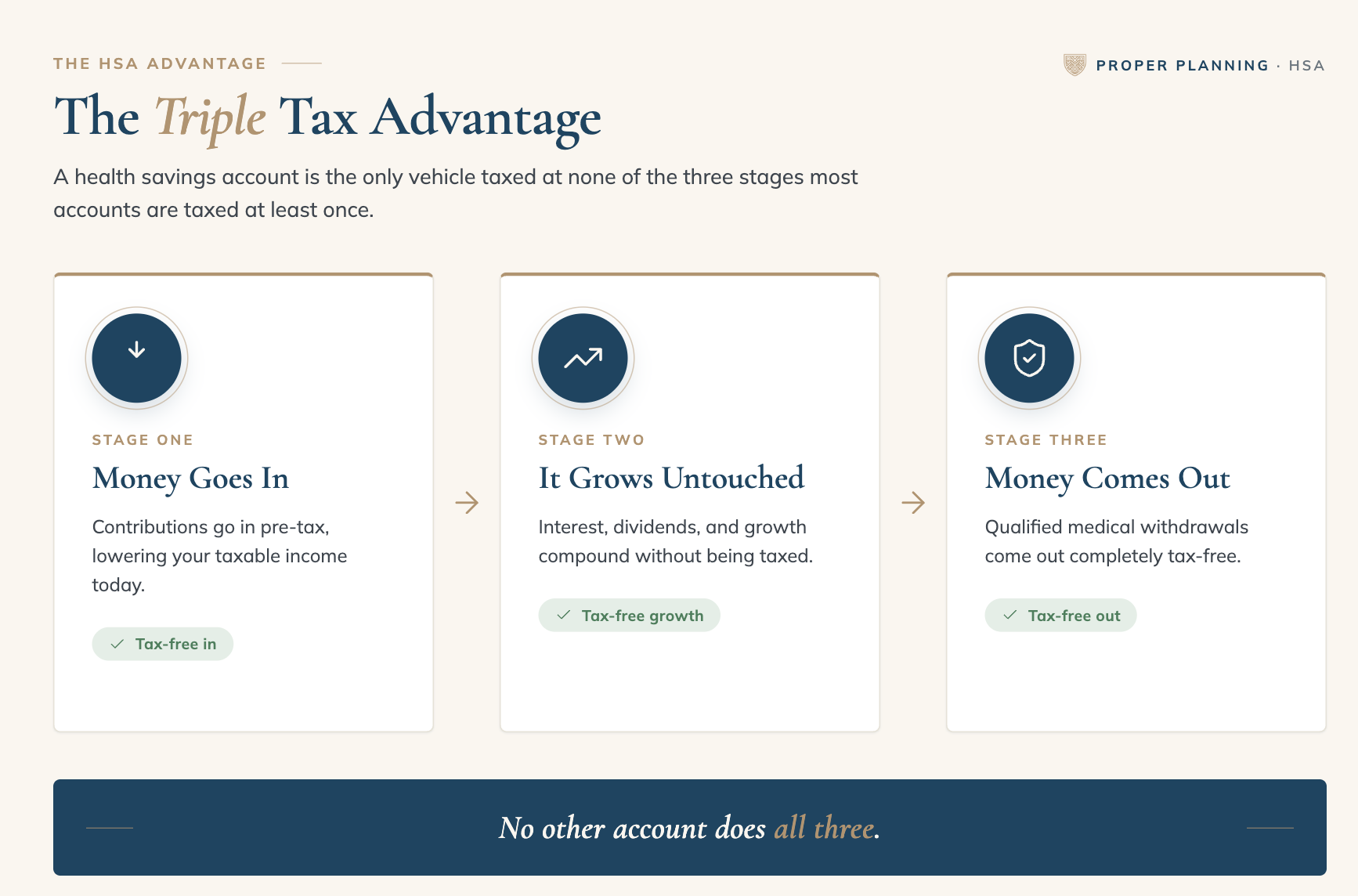

The HSA Is Your Most Underrated Account

If I could change one thing about how Garmin employees think about their benefits, it would be the Health Savings Account. When you elect the high-deductible health plan, you pay nothing in premiums and Garmin contributes $1,000 a year to your HSA. Most people treat that account as a place to pay for this year's doctor visits. That is a missed opportunity.

The HSA is the only account in the tax code with a triple tax advantage. Contributions are deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free as well. If you can afford to cover current medical costs out of pocket and let the HSA balance grow and stay invested, it becomes one of the most powerful retirement accounts you have. I regularly help clients shift their thinking from "medical spending account" to "highly advantaged retirement account."

RSUs and Other Benefits Worth a Look

If you receive restricted stock units, plan ahead for the tax hit. RSUs are taxed as ordinary income when they vest, and I have watched employees get caught off guard by a larger tax bill than they expected simply because they did not see it coming.

A couple of other benefits are easy to overlook. Garmin's tuition reimbursement program is worth serious consideration if you are early in your career and building skills that could accelerate your growth. And families who skip the dependent care FSA during open enrollment are leaving pre-tax dollars on the table for childcare they are already paying for.

The Concentration Risk Nobody Talks About

This is the challenge I see most often. Between the ESPP and RSUs, an employee who has been at Garmin for several years can end up with a large share of their net worth tied to a single stock. It feels natural. You believe in the company, you use the products, and the stock has treated you well. But when your paycheck, your retirement savings, and a concentrated stock position are all connected to the same employer, that is a real vulnerability.

I once worked with a client who had been with Garmin more than a decade, contributed to the ESPP the entire time, and never sold a share. More than half of their investable assets were in Garmin stock. We built a disciplined plan to diversify a portion each quarter while being thoughtful about the tax impact of selling shares with different cost bases and holding periods. The lesson I share with everyone…Being a loyal employee and being a diversified investor are not mutually exclusive.

If You Are Thinking About Leaving

A few items are time-sensitive enough that I encourage people to talk through them well before giving notice. Check your ESPP enrollment period, because walking away mid-cycle can mean forfeiting that 15% discount. Understand what happens to any unvested RSUs, since you may lose them entirely, and the math can favor staying a few extra weeks. And map out your health coverage transition so there is no gap between plans. Your HSA, by the way, is yours to keep no matter where you work.

Planning for Retirement

The shift from a steady paycheck to drawing on your savings is one of the bigger transitions a person goes through. I break it into a few steps: understand what you actually spend, map out your guaranteed income sources including Social Security and the optimal timing to claim it, and then build a withdrawal strategy. This is where employees who have been strategic throughout their career have a real advantage. Having a mix of pre-tax (401k), post-tax (Roth*), and tax-free (HSA) money gives us the flexibility to manage your tax bracket year by year in retirement.

A Note for Highly Compensated Employees

Higher pay adds planning layers. Employees and executives with significant RSUs need a clear strategy for the tax hit at vesting and for diversifying those shares over time. A large vest can push you into a higher bracket, affect how your Social Security is taxed if you are nearing retirement, or trigger the Net Investment Income Tax. Higher earners also tend to reach 401k contribution limits sooner, which opens the conversation around backdoor Roth contributions, a mega backdoor Roth where the plan allows, and taxable accounts. These are decisions that reward proactive planning rather than after-the-fact reactions.

One Local Wrinkle

Garmin is headquartered in Olathe, and our metro straddles the Kansas-Missouri line. The two states treat income, property, and retirement income differently, so where you live can affect both your take-home pay today and your tax picture in retirement. If you are nearing retirement and considering a move within the metro, that state line is definitely worth modeling out.

The Bottom Line

Garmin's benefits are generous, but they are also complex, and the pieces interact in ways that are easy to miss when you are making decisions in isolation during open enrollment. The question I encourage employees to ask is not "am I doing something wrong" but "am I capturing everything available to me." Most people, even those who have managed their money well on their own, find at least one meaningful opportunity they had been missing.

If you work at Garmin and want a second set of eyes on how your benefits fit into your broader plan, let’s talk.

*Traditional IRA account owners have considerations to make before performing a Roth IRA conversion. These primarily include income tax consequences on the converted amount in the year of conversion, withdrawal limitations from a Roth IRA, and income limitations for future contributions to a Roth IRA. In addition, if you are required to take a required minimum distribution (RMD) in the year you convert, you must do so before converting to a Roth IRA. Proper Planning & Wealth Management and LPL Financial do not provide legal advice or tax services. Please consult your legal advisor or tax advisor regarding your specific situation.

This material is for general information and educational purposes only and is not intended to provide specific advice or recommendations for any individual. Investing involves risk including the loss of principal. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.