The Most Powerful Account You're Probably Using Wrong

Most people treat their Health Savings Account (HSA) like a glorified checking account. Money goes in, a copay or a prescription comes out, and the balance hovers near zero by December. That is a missed opportunity, because the HSA is the only account in the entire tax code that gives you a tax break on the way in, on the way through, and on the way out. Used deliberately, it can become one of the most efficient retirement assets you own.

Here is how it works, and how a little discipline can turn a modest health account into a meaningful tax-free nest egg.

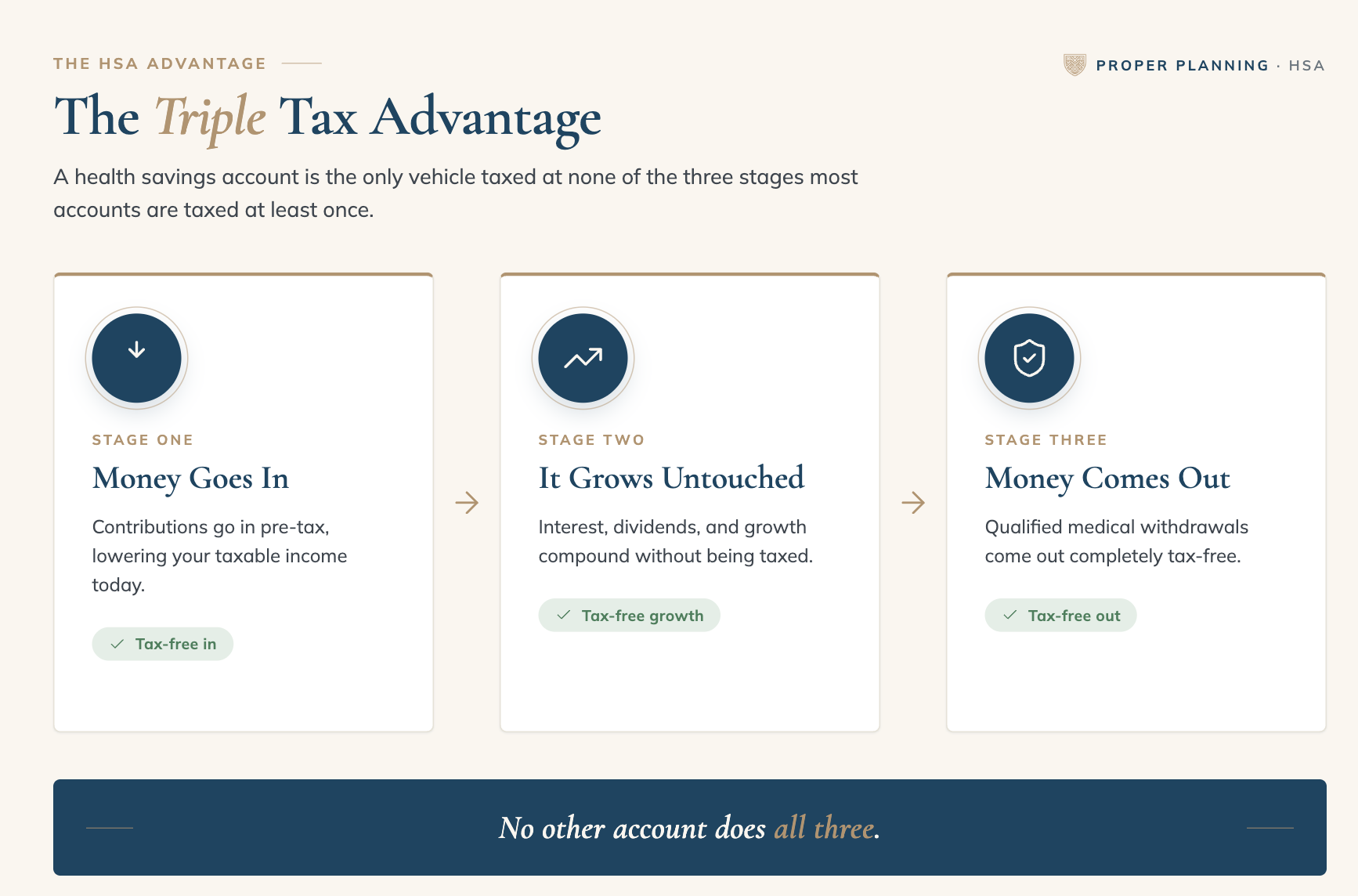

Three tax breaks in one account

The HSA earns the label "triple tax-free" because it delivers three distinct advantages that no other account combines:

Your contributions go in tax-free, and wether you contribute through your employer or make a contribution and deduct it later, the money reduces your taxable income for the year.

Your growth is never taxed. Once you have enough in the account, most HSA custodians let you invest the balance in mutual funds or other holdings. Those earnings compound year after year with no tax drag.

Your qualified withdrawals come out tax-free. You pay no taxes when you use the money for eligible medical costs.

Compare that to your other accounts. A 401k or traditional IRA gives you the deduction now but taxes every dollar you withdraw later. A Roth taxes you now so you can withdraw tax-free later. The HSA is the only one that avoids tax at every single stage.

Who can contribute, and how much

To fund an HSA you must be covered by an HSA-eligible high deductible health plan ("HDHP") and carry no other coverage that could disqualify you. For 2026, that plan must have a minimum deductible of at least $1,700 for individual coverage or $3,400 for family coverage.

The 2026 contribution limits are $4,400 for self-only coverage and $8,750 for family coverage. If you are 55 or older, you can add a $1,000 catch-up contribution on top.

One important caveat to know in advance... Enrolling in Medicare ends your ability to contribute to an HSA. If you plan to work past 65, that timing deserves a conversation before you sign up.

The rules that decide whether a withdrawal is tax-free

Money used for qualified medical costs is always tax-free and penalty-free, at any age.

Money used for anything else before age 65 is taxed as ordinary income and hit with an additional 20 percent penalty.

Money used for anything else after age 65 is still taxed as ordinary income, but the 20 percent penalty disappears.

Read that last point again, because it is the quiet superpower of the HSA! After 65, a non-medical withdrawal works exactly like a traditional IRA distribution. So the HSA behaves like a Roth when you use it for health costs and like a traditional IRA when you use it for anything else. You are not locked into one or the other. You get to decide later.

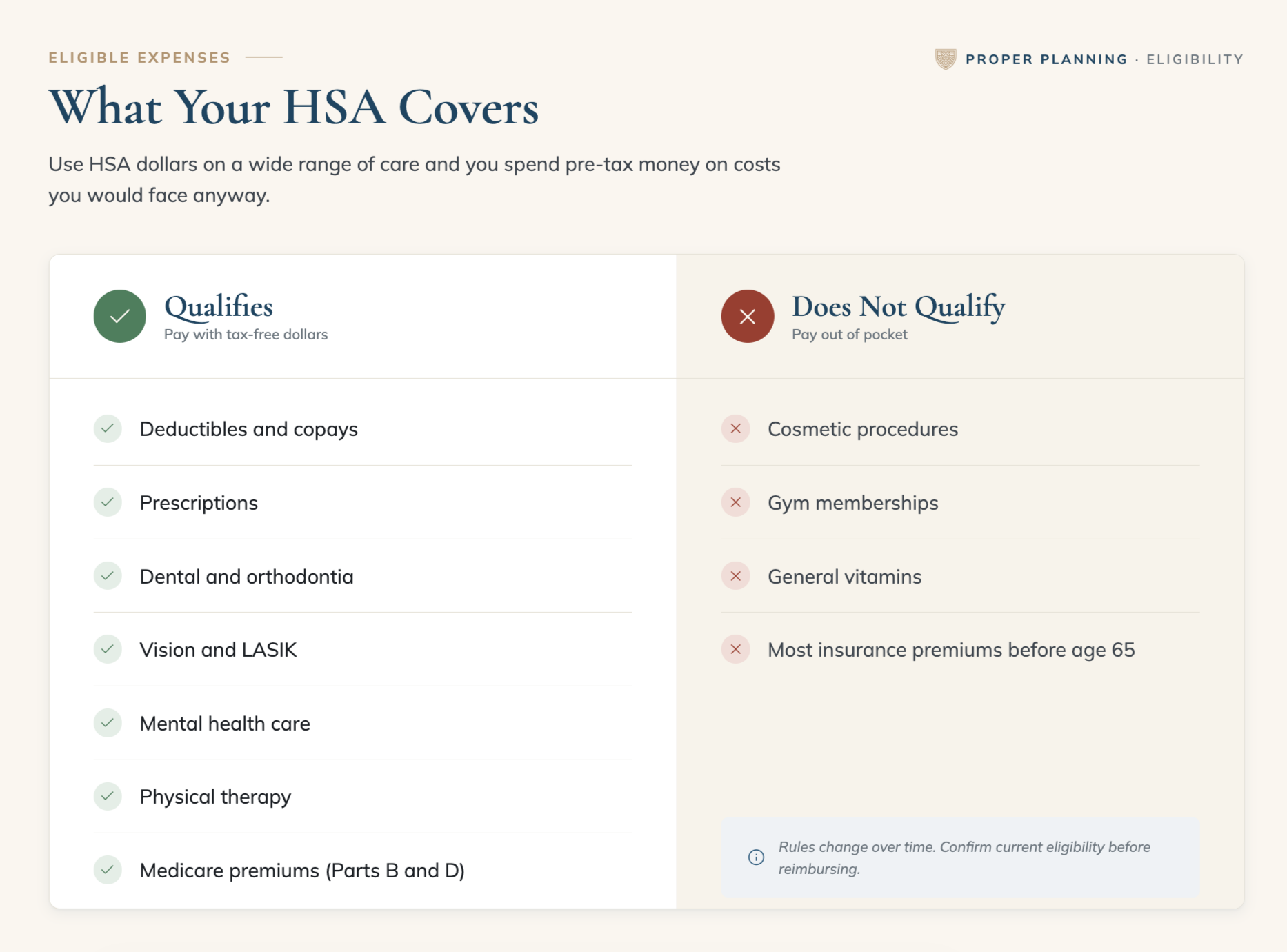

What actually qualifies

Qualifying costs include deductibles and copays, prescriptions, dental work and orthodontia, vision care and LASIK, mental health care, physical therapy, certain long-term care costs, and, once you reach 65, Medicare premiums for Parts B and D and Medicare Advantage. Qualified long-term care insurance premiums also count, up to certain age-based limits.

Some things do not qualify.. Cosmetic procedures, gym memberships, general daily vitamins, and most health insurance premiums before age 65 fall outside the rules. The eligibility list does shift over time, so it is always worth confirming a cost before you reimburse against it.

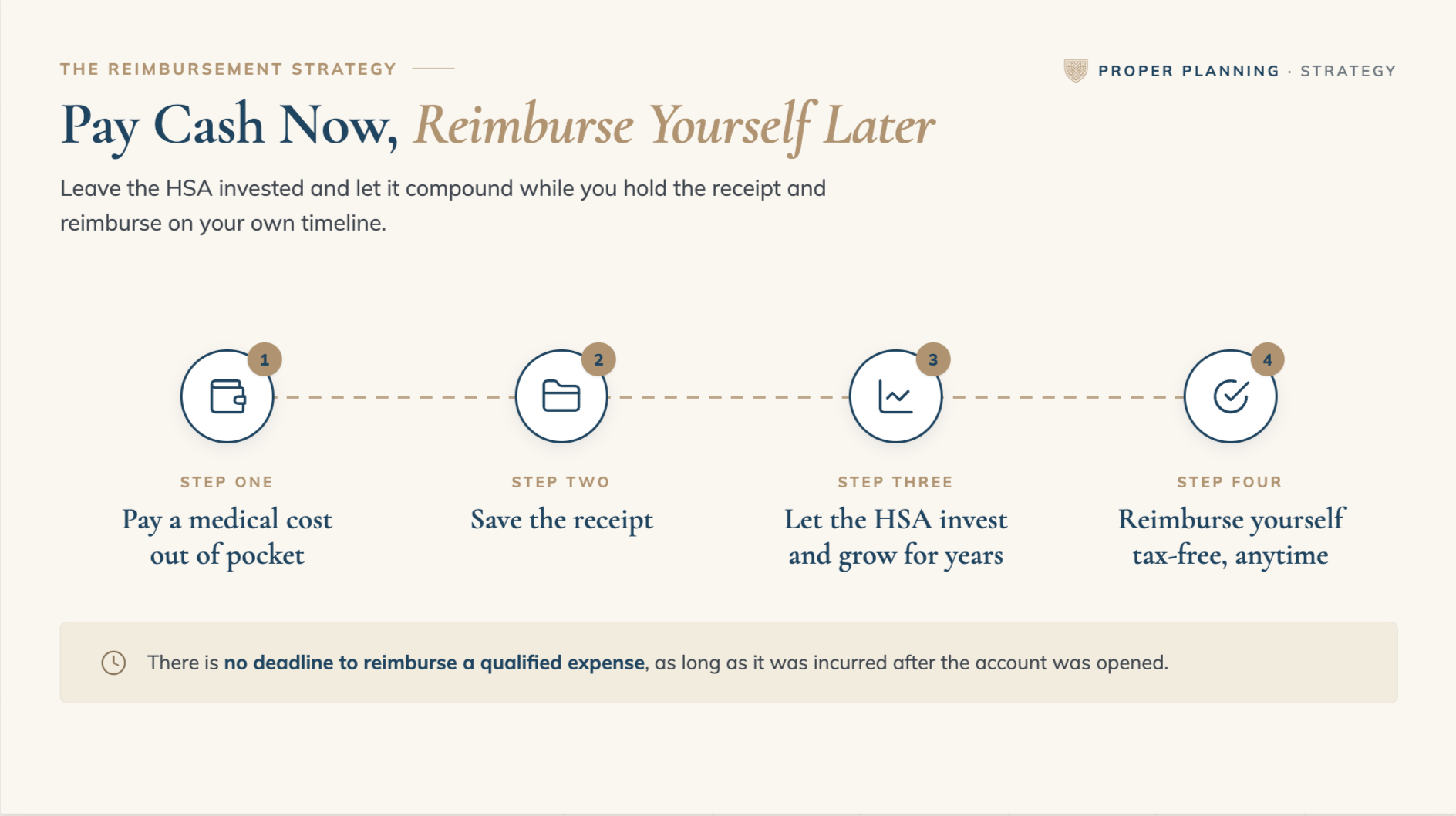

Pay cash now, reimburse yourself later

Here is the strategy that separates people who use an HSA from people who use it well.

There is no deadline to reimburse yourself for a qualified medical cost. As long as the cost was incurred after you opened the HSA, you have not already reimbursed it, and you have not deducted it elsewhere on your taxes, you can pay for it out of pocket today and reimburse yourself from the HSA years or even decades later.

That single rule changes everything. Instead of draining the account every time you visit the dentist, you pay those costs with regular cash, save the receipt, and leave the HSA invested. Next, start to accumulate a growing stack of unreimbursed receipts. Save the receipt every time you make a purchase with cash that would otherwise be covered by your HSA. Each receipt you save is essentially a tax-free withdrawal you are entitled to take whenever you want it!

When you reach retirement --or any point you need the money-- you can reimburse yourself for that entire backlog in one tax-free lump sum. Or draw it out how you see fit. In the meantime, your contributions have been growing tax-free the whole time. You have effectively turned the HSA into a tax-free growth account with a trapdoor you can pull at any time.

But remember that you will need to keep up on the recordkeeping. This strategy only works if you keep clean records of every qualified cost you paid out of pocket. A dedicated digital folder (iCloud / Dropbox / Google Drive etc.), or a receipt-tracking app makes this easy and protects you.

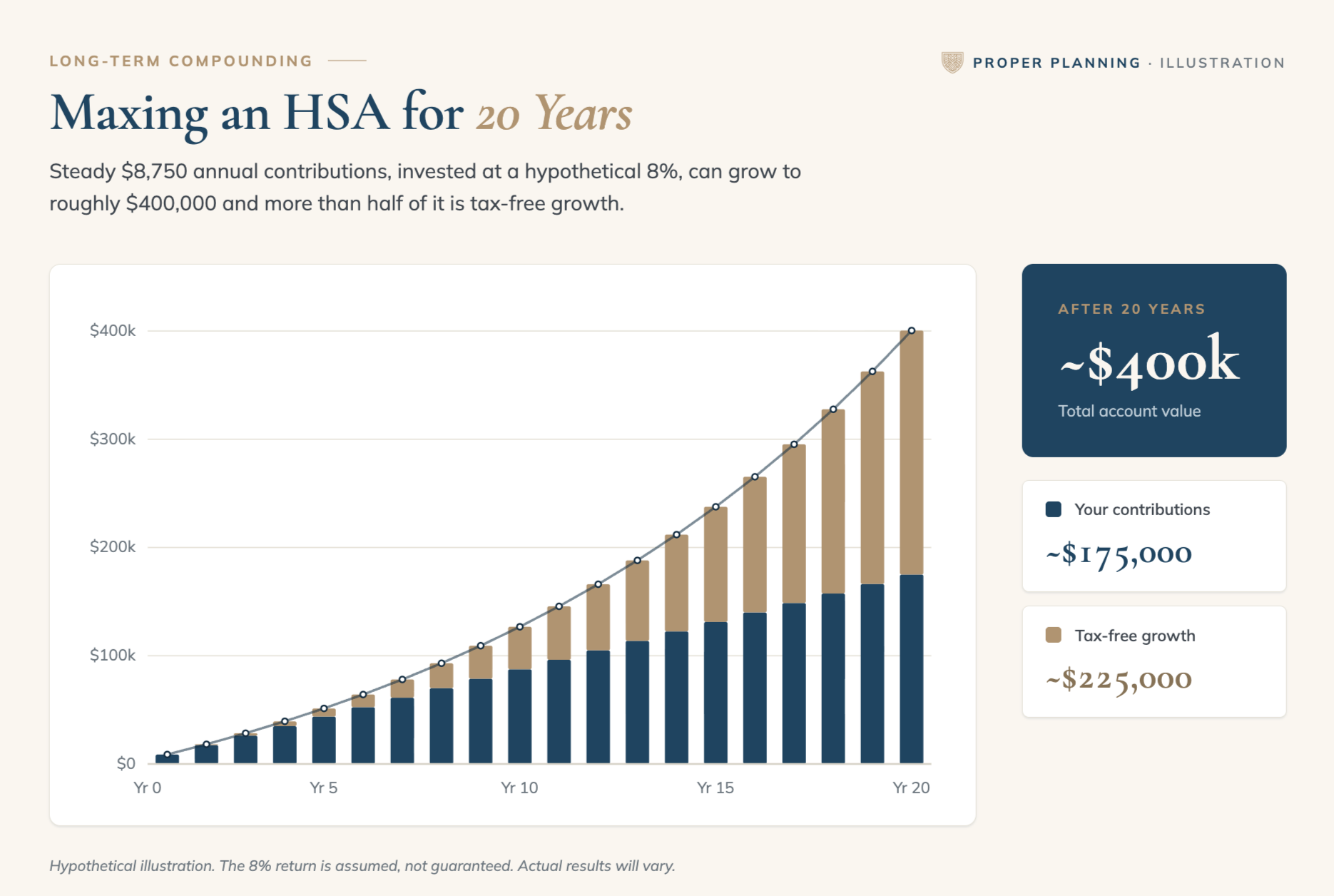

What the math looks like

The numbers make the case better than words do. Suppose a family maxes the HSA at $8,750 per year and invests it at a hypothetical 8 percent annual return. After 20 years the account grows to roughly $400,000. Of that, about $175,000 is your own contributions and about $225,000 is growth that is never taxed, as long as it ultimately covers qualified costs.

An individual maxing the $4,400 limit on the same assumptions lands near $201,000 after 20 years. And because the contribution limits rise with inflation over time, these figures likely understate what a disciplined saver would actually accumulate.

Who this fits, and who it does not

The receipt strategy assumes one thing above all: that you can comfortably pay your current medical costs out of pocket without touching the HSA. If covering a deductible out of cash flow would create real strain, then using the HSA as intended for current costs is the right call. The tax-free withdrawal still applies, and the account is still doing its job.

This is also a strategy that rewards a long runway. The longer the money stays invested, the more the tax-free growth compounds, and the more powerful the eventual reimbursement becomes. For someone a few years from needing the funds, the benefit is smaller.

The HSA rewards people who can be patient and organized. If that describes you, it may be the most undervalued account on your statement.

Ready to build your financial plan with us?

This material is for general informational and educational purposes only and is not intended as individualized tax, legal, or investment advice. The hypothetical example assumes an 8 percent annual return for illustrative purposes only. It is not representative of any specific investment and does not reflect the deduction of any costs or taxes. Actual results will vary. Investing involves risk including possible loss of principal, and no strategy assures success or protects against loss. HSA eligibility, contribution limits, and qualified expense rules are subject to change. Consult a qualified tax or financial professional regarding your specific situation.