Tax Strategy Is a Year-Round Game: What Smart Planners Do Differently

With April approaching, taxes are top of mind for most people. But here is an uncomfortable truth: if the first time you think about your tax situation each year is when your CPA sends you a questionnaire, you are almost certainly paying more than you need to.

In our previous article, What a Real Financial Plan Actually Looks Like, we touched on the idea that tax planning should be proactive, not reactive. Today, we are going to unpack that idea in detail and walk through several strategies that can meaningfully reduce your tax burden over time. Some of these are straightforward. Others are more advanced. All of them require planning well before April 15.

Roth Conversions: Paying Taxes Now to Save More Later

A Roth conversion* involves moving money from a traditional IRA or 401(k) into a Roth IRA. You pay income tax on the converted amount in the year you do it, but from that point forward, the money grows tax-free and qualified withdrawals in retirement are completely tax-free as well.

The question is not whether Roth conversions are a good idea in general. The question is whether they make sense for you, right now, given your specific circumstances.

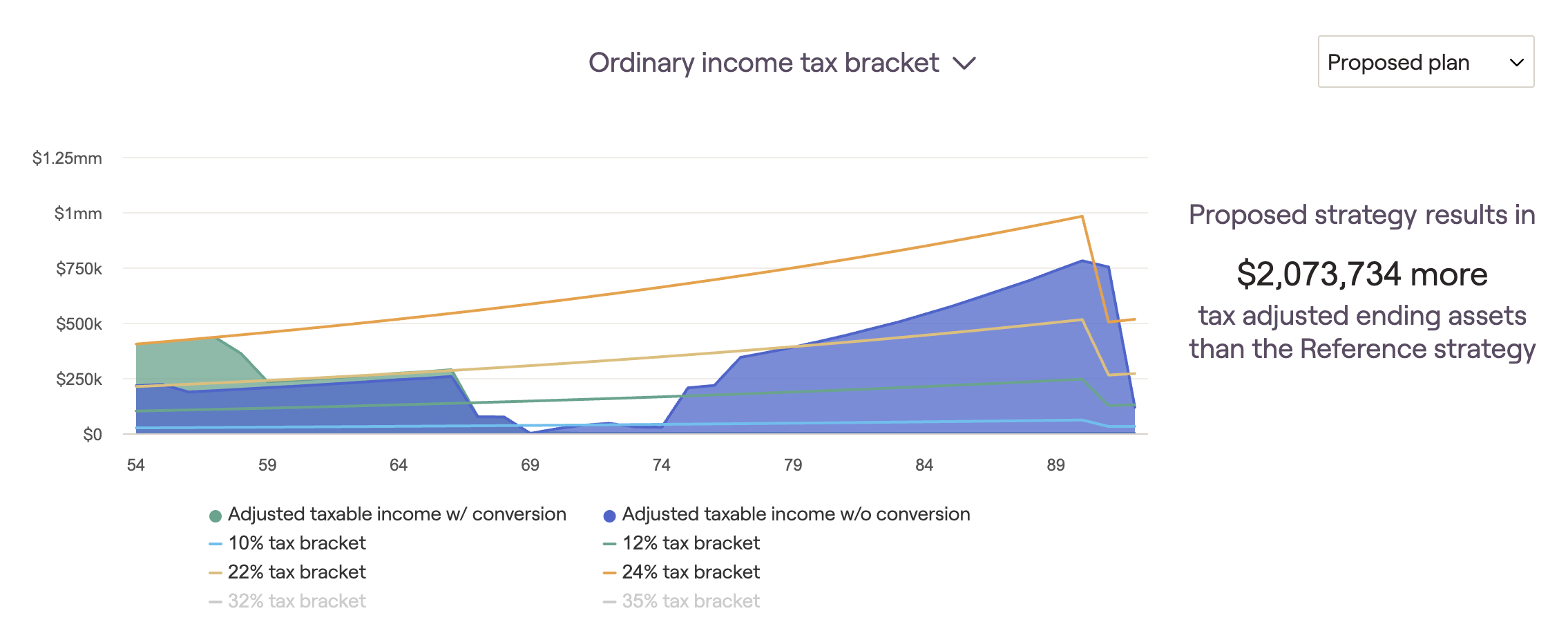

Roth conversions tend to be most valuable in years when your taxable income is unusually low. That might happen during a gap between jobs, a year of heavy business losses, the early years of retirement before Social Security and Required Minimum Distributions kick in, or a year when you have large deductions. In these situations, you can convert at a lower tax bracket than you would otherwise pay in the future.

The strategy gets more nuanced from there. How much should you convert? You generally want to "fill up" your current tax bracket without pushing yourself into the next one. Should you convert all at once or spread it over several years? A multi-year conversion plan often yields better results than a single large conversion. What about the impact on Medicare premiums? IRMAA surcharges can catch people off guard two years after a large conversion. These are the kinds of details that require careful modeling, not a quick rule of thumb.

Tax-Loss Harvesting (and Its Lesser-Known Cousin, Gain Harvesting)

Tax-loss harvesting is a strategy most investors have heard of, at least in concept. When an investment in a taxable account has declined in value, you sell it to realize the loss, then reinvest the proceeds in a similar (but not "substantially identical") holding to maintain your market exposure. The realized loss offsets capital gains elsewhere in your portfolio, and if your losses exceed your gains, you can deduct up to $3,000 per year against ordinary income, carrying the rest forward.

What gets less attention is the importance of doing this systematically throughout the year, not just in December. Market volatility creates harvesting opportunities at unpredictable times. An advisor who is monitoring your portfolio regularly can capture losses as they appear, building up a bank of tax losses that can be deployed strategically for years to come.

The wash sale rule is the main trap to watch for here. If you buy a substantially identical security within 30 days before or after the sale, the loss is disallowed. This applies across all of your accounts, including IRAs, so coordination matters.

Now, what about gain harvesting? This is a strategy that often surprises people. In years when your income is relatively low, you may find yourself in the 0% long-term capital gains bracket. That means you can sell appreciated investments, realize the gain, and pay zero federal tax on it. You then repurchase the same investment immediately (no wash sale rule for gains) at a higher cost basis. The result is that you have effectively locked in gains tax-free and reset your cost basis, reducing future tax liability.

This can be especially powerful for retirees in their early 60s who have not yet started Social Security, or for anyone experiencing a temporary dip in income. It is a window of opportunity that does not stay open forever.

Donor-Advised Funds: Charitable Giving with Strategic Flexibility

A Donor-Advised Fund, or DAF, is one of the most flexible and tax-efficient charitable giving vehicles available. You make an irrevocable contribution to the fund (in cash, securities, or other assets), receive an immediate tax deduction, and then recommend grants to your favorite charities over time. Meanwhile, the assets in the fund can be invested and grow tax-free.

The strategic power of a DAF lies in its ability to separate the timing of the tax deduction from the timing of the charitable gift. This opens the door to a technique known as "bunching." Under current tax law, the standard deduction is high enough that many people no longer benefit from itemizing. But if you contribute two or three years' worth of charitable giving into a DAF in a single year, you may push your itemized deductions above the standard deduction threshold, capturing a real tax benefit. In the off years, you simply take the standard deduction while continuing to distribute grants from the fund.

DAFs are also an excellent vehicle for donating appreciated stock. When you contribute shares that have gained value, you avoid the capital gains tax entirely and receive a deduction for the full fair market value. Compared to selling the stock, paying the tax, and donating the cash, this approach can put significantly more money to work for the causes you care about.

Charitable Remainder Trusts: Income, Tax Savings, and Legacy in One Structure

For clients with larger portfolios and charitable intent, a Charitable Remainder Trust (CRT) can be a remarkably powerful planning tool. A CRT allows you to transfer appreciated assets into an irrevocable trust. The trust then sells the assets with no immediate capital gains tax, reinvests the full proceeds, and pays you (or another beneficiary) an income stream for a set period of years or for life. When the trust term ends, the remaining assets go to the charity or charities of your choice.

The tax benefits are layered. First, you receive a partial income tax deduction in the year you fund the trust, based on the estimated present value of the future charitable gift. Second, the trust itself is tax-exempt, so the appreciated assets can be sold and reinvested without the drag of capital gains tax. Third, the income you receive from the trust is taxed according to a tiered system that spreads different types of income (ordinary, capital gains, tax-exempt) over the payout period, which can result in favorable treatment compared to selling the assets outright.

CRTs come in two main flavors: a Charitable Remainder Annuity Trust (CRAT), which pays a fixed dollar amount each year, and a Charitable Remainder Unitrust (CRUT), which pays a fixed percentage of the trust's value, recalculated annually. A CRUT is more common because the income stream adjusts with the trust's performance, offering a natural hedge against inflation.

One scenario where CRTs shine: a business owner who has just sold a company and is sitting on a large capital gain. Funding a CRT with the proceeds can defer and spread the tax impact while providing a steady income stream during retirement.

Irrevocable Life Insurance Trusts: Keeping Insurance Proceeds Out of Your Estate

Most people do not realize that life insurance proceeds, while income-tax-free to the beneficiary, are included in your taxable estate for federal estate tax purposes. For families with larger estates, this can create a significant and sometimes unexpected tax bill.

An Irrevocable Life Insurance Trust, or ILIT, solves this problem. Instead of you owning the policy directly, the ILIT owns it. When you pass away, the death benefit is paid to the trust and distributed to your beneficiaries completely free of both income tax and estate tax.

Setting up an ILIT requires careful attention to detail. The trust must be the owner and beneficiary of the policy from the start (or, if you transfer an existing policy, you need to survive the transfer by at least three years for it to be excluded from your estate). Premium payments are typically funded through annual gifts to the trust, which require "Crummey" notices to the beneficiaries to qualify for the annual gift tax exclusion.

ILITs are especially valuable in two situations. The first is estate liquidity: if your estate is heavy in illiquid assets like real estate or a closely held business, the insurance proceeds held in the ILIT can provide cash to cover estate taxes, legal fees, and other expenses without forcing a fire sale. The second is wealth transfer: when paired with strategies like CRTs, an ILIT can replace the charitable gift with tax-free insurance proceeds for your heirs, effectively allowing you to have your cake and eat it too.

How These Strategies Work Together

The real power of tax strategy is not in any single technique. It is in how these tools are coordinated within a comprehensive financial plan. Consider a simplified example:

A couple in their early 60s sells a family business for a substantial gain. They contribute a portion of the business interest into a CRT before the sale, deferring the capital gains hit and creating a retirement income stream. They use a DAF to bunch several years of charitable giving into the sale year, maximizing their deduction when their income is highest. They contribute appreciated stock from their taxable portfolio into the DAF to avoid capital gains on those shares. They establish an ILIT to replace the charitable remainder with tax-free insurance proceeds for their children. And over the next several years, they execute a series of Roth conversions during the gap before Social Security and RMDs begin, filling up lower tax brackets with converted dollars that will grow tax-free for the rest of their lives.

No single piece of this plan works in isolation. The CRT reduces the current tax hit. The DAF and appreciated stock donation amplify the deduction. The ILIT preserves the family legacy. The Roth conversions reduce future tax exposure. Together, they form a coordinated strategy that dramatically reduces the family's lifetime tax burden while supporting their charitable goals and protecting their heirs.

That is what proactive tax planning looks like.

Do Not Wait Until April

If there is one takeaway from this article, it is this: the best tax strategies require time. Roth conversions need to be modeled before year-end. Loss harvesting works best when monitored continuously. CRTs and ILITs take months to set up properly. DAF contributions need to happen before December 31 to count for the current tax year.

April is for filing. The real planning happens in the months and years before that. If your current approach to taxes is purely reactive, you are almost certainly leaving significant savings on the table.

The strategies described here are not reserved for the ultra-wealthy. Many of them, particularly Roth conversions, loss harvesting, gain harvesting, and DAFs, are accessible to a wide range of investors. The key is having an advisor who thinks about your tax picture holistically and plans ahead, not one who only looks backward at last year's return.

Wondering how much proactive tax strategy could save you?

Schedule a complimentary consultation and let us take a closer look at your tax picture.

* Traditional IRA account owners have considerations to make before performing a Roth IRA conversion. These primarily include income tax consequences on the converted amount in the year of conversion, withdrawal limitations from a Roth IRA, and income limitations for future contributions to a Roth IRA. In addition, if you are required to take a required minimum distribution (RMD) in the year you convert, you must do so before converting to a Roth IRA. Contributions to a traditional IRA may be tax deductible in the contribution year, with current income tax due at withdrawal. Withdrawals prior to age 59 ½ may result in a 10% IRS penalty tax in addition to current income tax. Proper Planning & Wealth Management and LPL Financial do not provide legal advice or tax services. Please consult your legal advisor or tax advisor regarding your specific situation.