What a Real Financial Plan Actually Looks Like

If you have ever sat down with a financial advisor and walked away with little more than a pie chart of your investment allocation, you are not alone. That experience is incredibly common, and it leaves a lot of people wondering whether financial planning is really worth the time and cost.

A pie chart is not a financial plan. A list of investments and percentages is not a financial plan. And a one-page printout from a software tool is not a financial plan.

A real financial plan is a living, breathing strategy that connects every major financial decision in your life to a set of clearly defined goals. It is not a product someone sells you. It is a process you work through with a trusted advisor, and it evolves as your life changes. Here is what that actually looks like in practice.

It Starts with Your Life, Not Your Money

A good financial plan does not begin with account balances or risk tolerance questionnaires. It begins with a conversation about your life. What does a great retirement look like to you? Are you planning to help your kids pay for college? Do you want to sell your business in ten years, or pass it to a family member? Are you worried about caring for aging parents?

These are the questions that shape everything else. Without them, we are just guessing at what to optimize. With them, every recommendation has a clear reason behind it. That clarity is the difference between a pricey plan that just sits in a drawer and one that actually guides your decisions.

A Clear Picture of Where You Stand Today

Before you can map a route, you need to know your starting point. A real financial plan includes a thorough inventory of your current financial life: income, expenses, assets, debts, insurance coverage, employee benefits, estate documents, and tax returns. Nothing gets left out.

This is where most people are surprised. They often discover gaps they did not know existed. Maybe your life insurance has not been updated since your first child was born. Maybe your 401(k) beneficiary designations still list an ex-spouse. Maybe you are sitting on a concentrated stock position without realizing the risk. A comprehensive review catches these things before they become expensive problems.

Cash Flow and Spending Analysis

You cannot build a meaningful plan without understanding how money moves through your household. This does not mean tracking every nickle (unless you want to). It means understanding, at a high level, where your income goes each month and whether your current spending patterns support or undermine your long-term goals.

A strong cash flow analysis often reveals opportunities that have nothing to do with investing. Sometimes the most impactful move is restructuring debt, adjusting your savings rate, or optimizing the timing of major expenses. These are practical, real-world adjustments that make a measurable difference.

Tax Strategy That Goes Beyond Filing

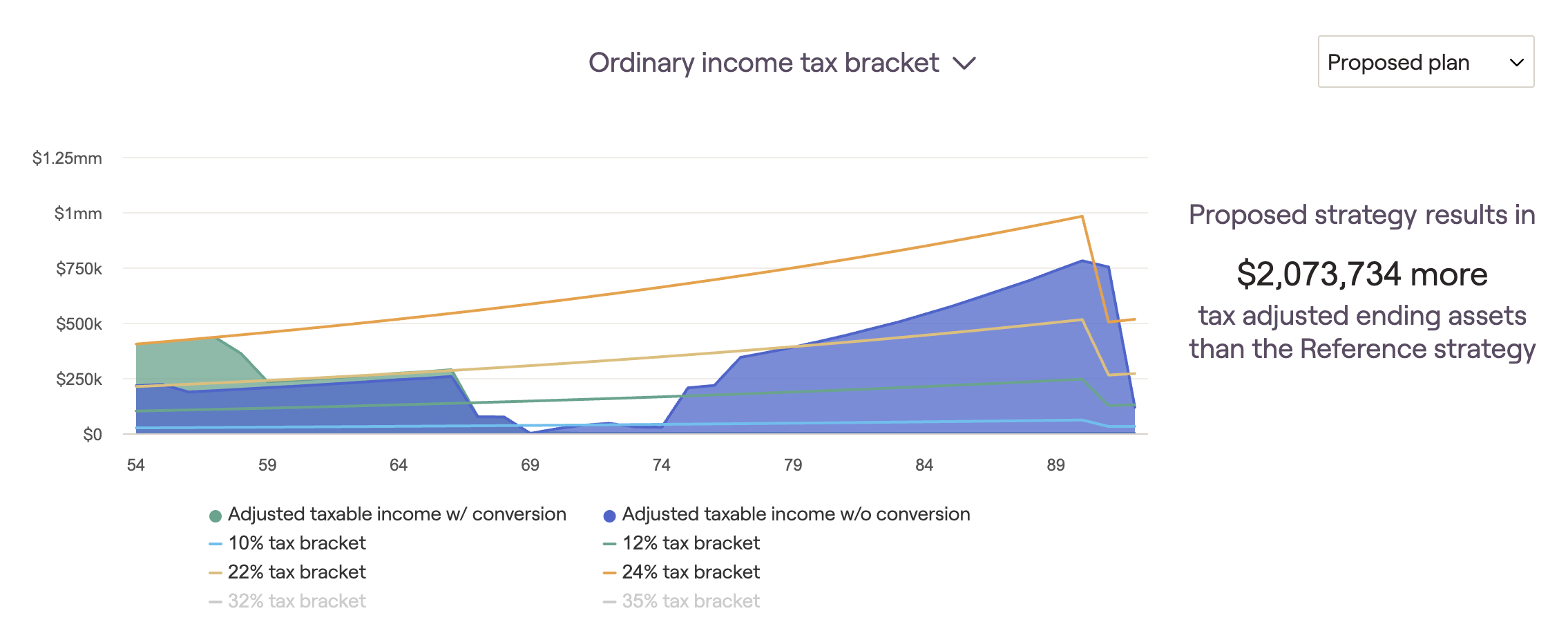

Tax planning is one of the most overlooked areas of financial planning, and it is also one of the most valuable. A real plan does not just help you file your returns. It looks ahead to minimize your lifetime tax burden through strategies like Roth conversions*, tax-loss harvesting, charitable giving structures, and smart timing of income and deductions.

For business owners, tax strategy gets even more layered. The way you structure your compensation, the type of retirement plan you use, and how you handle business expenses can all have a significant impact. This is especially true for S corporation owners who need to balance reasonable compensation against distributions.

The key point is that tax planning should be proactive, not reactive. If you are only thinking about taxes in April, you are leaving money on the table.

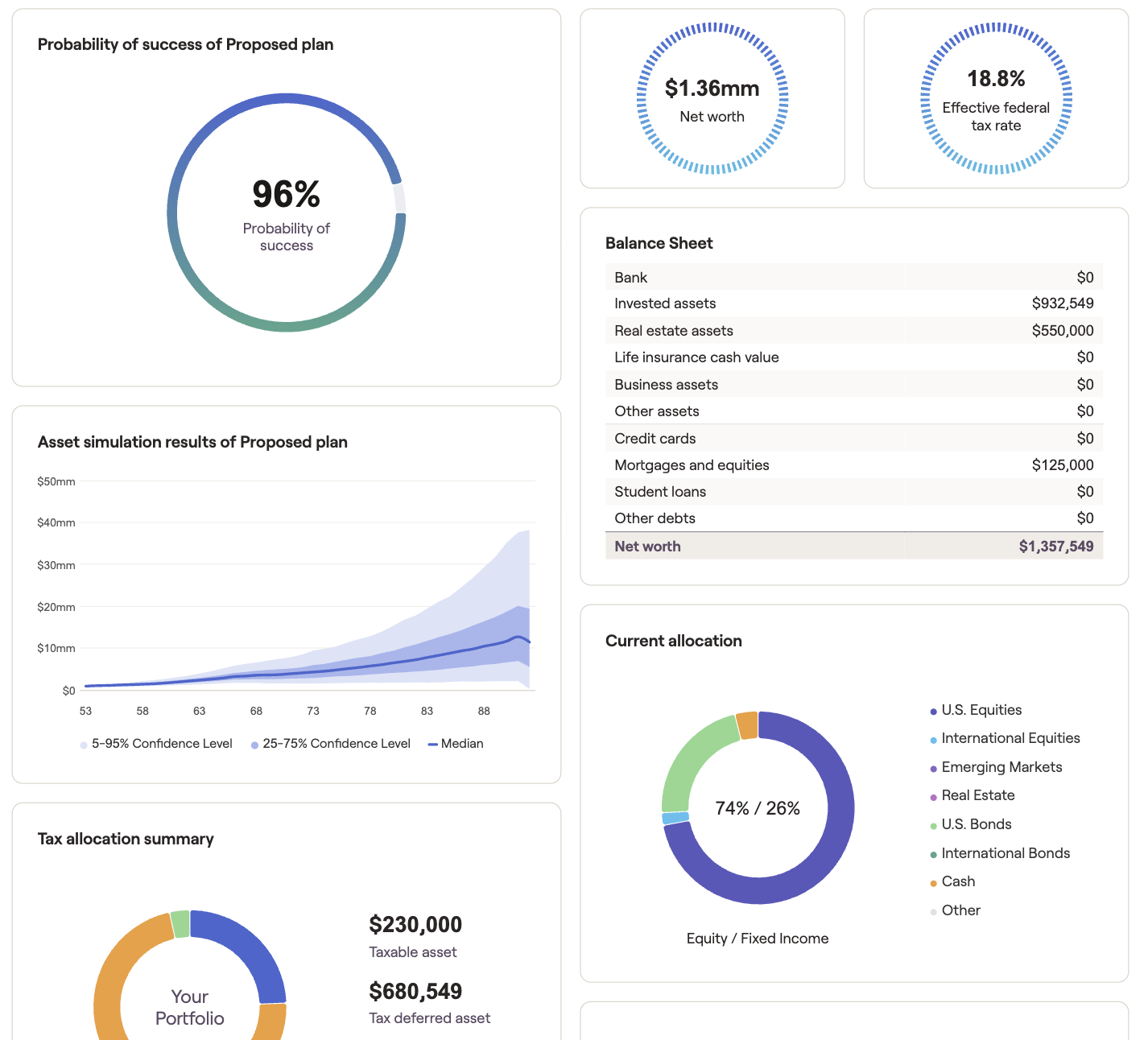

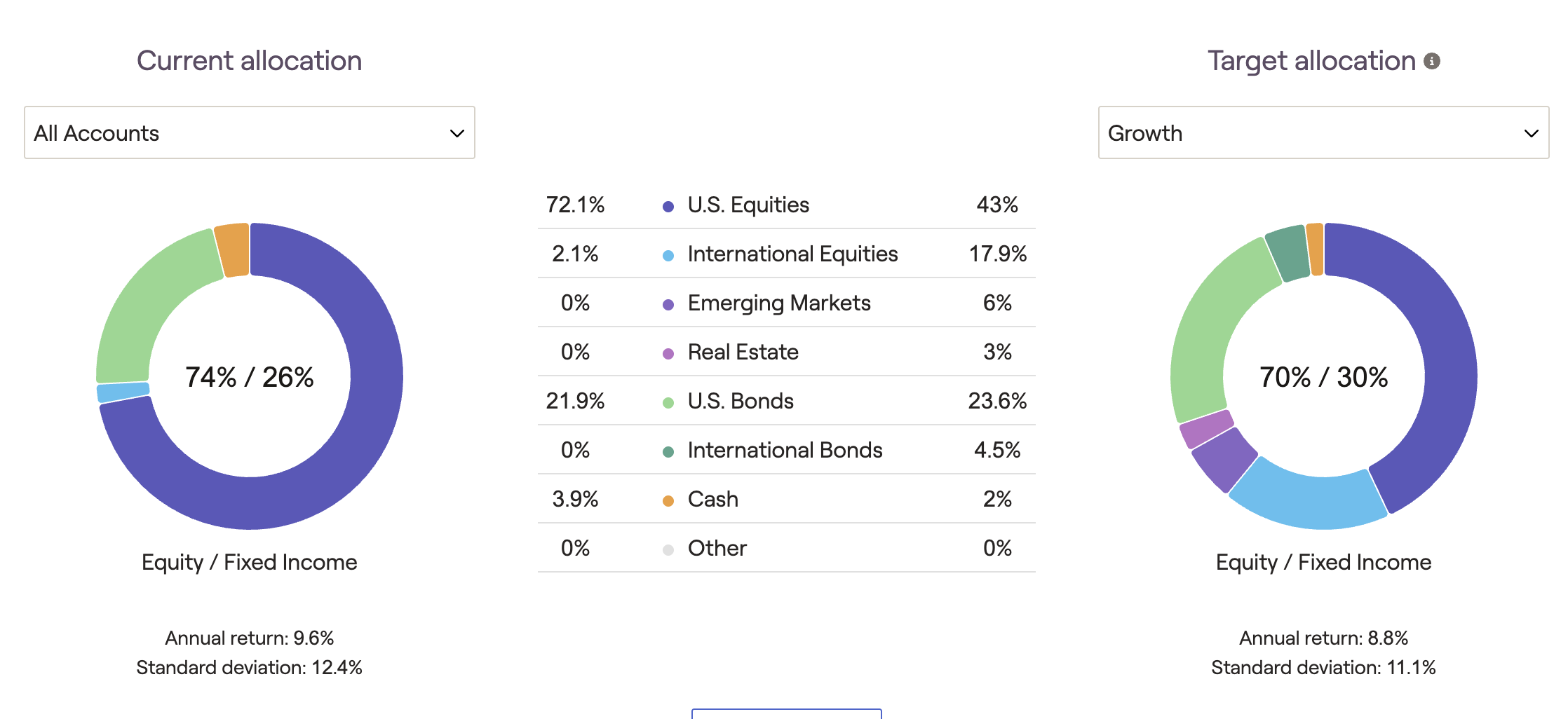

Investment Management in Context

Yes, investments are part of a financial plan. But in a real plan, your investment strategy is built to serve your goals, not the other way around. That means your portfolio is designed around when you need the money, how much risk you can actually afford to take (not just how much volatility you can tolerate), and how your investments interact with the rest of your financial picture.

If you own a business in the energy sector, loading your portfolio with energy stocks creates concentration risk you might not see at first glance. If all your savings is tied up in your company’s stock, that is concentration risk. If you are planning a major purchase in two years, that money should not be exposed to the same risk as your retirement savings. A good plan accounts for these connections.

Estate Planning and Wealth Transfer

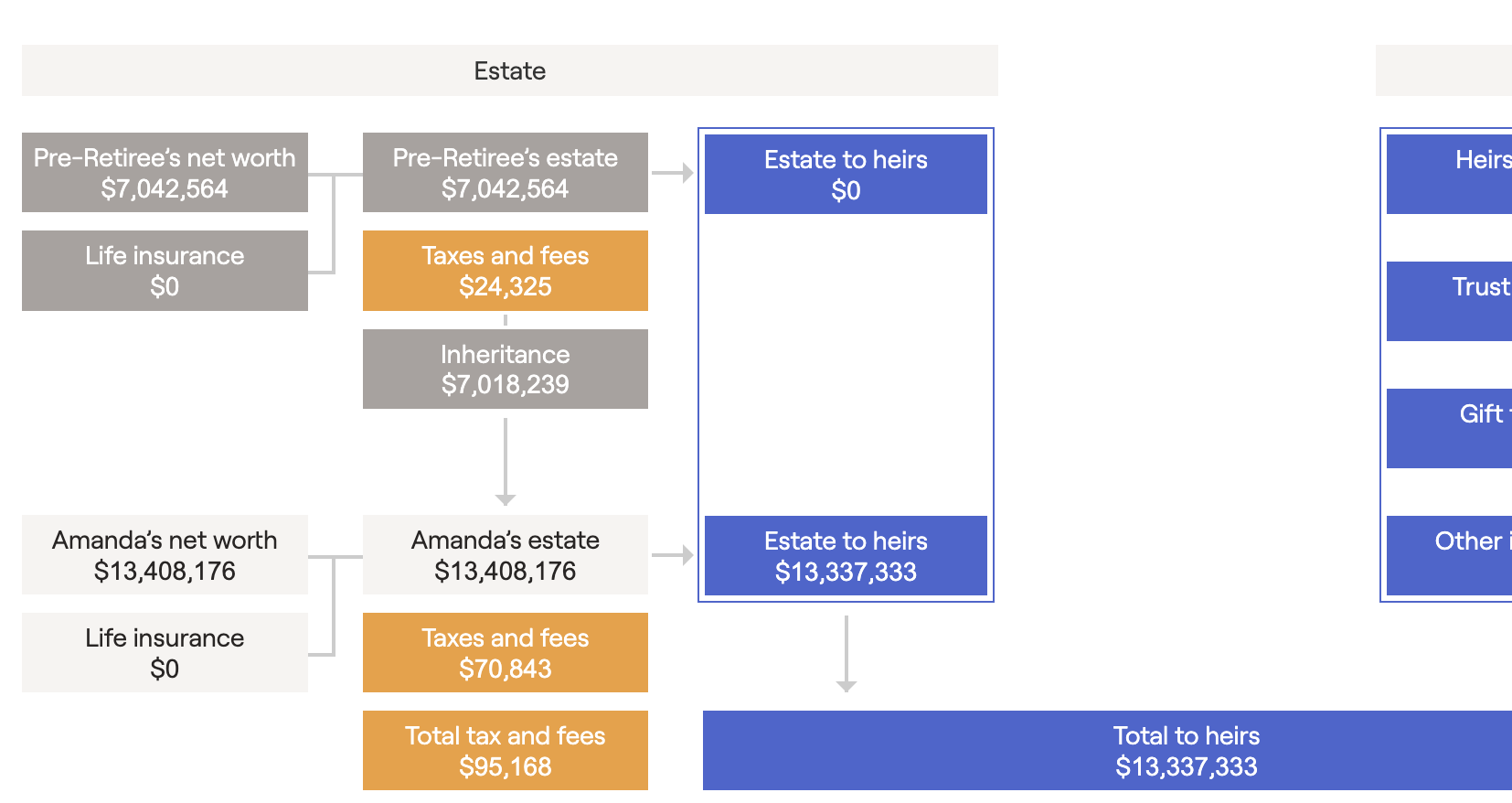

A financial plan that ignores estate planning is incomplete. Your estate plan is the bridge between the wealth you build during your lifetime and the legacy you leave behind. It includes wills, trusts, powers of attorney, healthcare directives, and beneficiary designations across all of your accounts.

What many people do not realize is how closely estate planning is tied to tax strategy. The way assets are titled, the structure of your trusts, and the timing of gifts can all affect how much of your wealth actually reaches the people and causes you care about. A real financial plan coordinates these pieces so that nothing falls through the cracks.

Risk Management and Insurance

No plan is complete without addressing the "what ifs." What happens to your family if you become disabled? What if you need long-term care? What if a lawsuit threatens your assets? Insurance is not glamorous, but it is the foundation that protects everything else in your plan.

A real plan reviews your coverage regularly and makes sure it evolves with your life. The insurance needs of a 35-year-old with young children are very different from those of a 60-year-old approaching retirement. If your coverage has not changed in a decade, there is a good chance it no longer fits.

It Is a Living Document, Not a One-Time Event

Perhaps the most important thing to understand about a real financial plan is that it is never "done." Life changes. Markets shift. Tax laws evolve. Your plan needs to keep pace with all of it.

A good wealth advisor does not hand you a plan and disappear. They meet with you regularly, review progress, adjust assumptions, and help you navigate decisions as they come up. Should you refinance? Is it time to exercise those stock options? Can you afford to retire early? These questions deserve more than a quick Google search or ChatGPT prompt. They deserve the attention of someone who knows your full financial picture.

The Bottom Line

A real financial plan is not a product. It is not a binder full of charts. It is a coordinated strategy that ties together your goals, your money, your taxes, your estate, and your protection into a single, coherent framework.

If you have never experienced that kind of planning, you might be surprised at how much clarity it brings. And if your current advisor is not delivering that level of depth, it may be time to ask why.

Ready to see what a proper financial plan looks like for you or your family?

Contact us today to schedule a complimentary consultation

* Traditional IRA account owners have considerations to make before performing a Roth IRA conversion. These primarily include income tax consequences on the converted amount in the year of conversion, withdrawal limitations from a Roth IRA, and income limitations for future contributions to a Roth IRA. In addition, if you are required to take a required minimum distribution (RMD) in the year you convert, you must do so before converting to a Roth IRA. Proper Planning & Wealth Management and LPL Financial do not provide legal advice or tax services. Please consult your legal advisor or tax advisor regarding your specific situation.